GCC petrochemicals producers need to rethink how they can achieve the scale of some of the larger international players

After enjoying 10 per cent annual output growth for a decade, the chemicals and petrochemicals sector in the GCC has run into headwinds.

Declining profitability, depressed margins and an erosion of traditional feedstock cost advantages are forcing regional producers to plot a new course through the fast-changing global petrochemicals market landscape.

The biggest annual gathering of chemicals professionals in the region in November heard urgent calls from industry leaders for greater integration, consolidation, joint investments into new technologies and more speciality chemicals.

Keeping our current structures is not suitable for the next decade, Yousef al-Benyan, vice-chairman and CEO of Saudi Basic Industries Corporation (Sabic) told the Gulf Petrochemicals & Chemicals Association (GPCA) forum in Dubai. We should see some mergers to be more competitive and we should consolidate to bring the industry to the next level.

As chairman of the GPCA, Al-Benyan is concerned about small and medium-sized producers and does not see a very bright future for the regions industry in its current state. The only way forward, he says, is to create synergies and optimise current assets. We dont have industry capital to leverage and to maintain the scale of competitiveness, he says.

Turbulent year

For the energy industry, 2015 was a turbulent year, with oil prices slumping more than 50 per cent from the mid-2014 peak of $115 a barrel. In a year when production volumes rose 3.2 per cent, a combination of the collapse in crude prices and slower economic growth caused global chemicals sales to dip by nearly 5 per cent to $3.92 trillion. GCC output accounted for 2 per cent of global sales, according to the GPCAs 2015 annual report.

Total GCC chemicals exports in 2015 declined by 2 per cent to 65.2 million tonnes. However, the drop in dollar terms was more pronounced, falling 21 per cent to $48.1bn as a result of price decreases and fluctuations in exchange rates. This was despite an overall 6 per cent rise in production capacity to 144.6 million tonnes. Total sales revenue was $79.7bn, down 9 per cent on 2014s value and the lowest level since 2012.

The ICIS Asian Petrochemical Index, which provides a capacity-weighted measure of the average change in prices for a basket of 12 key products, has fallen by a third since July 2014.

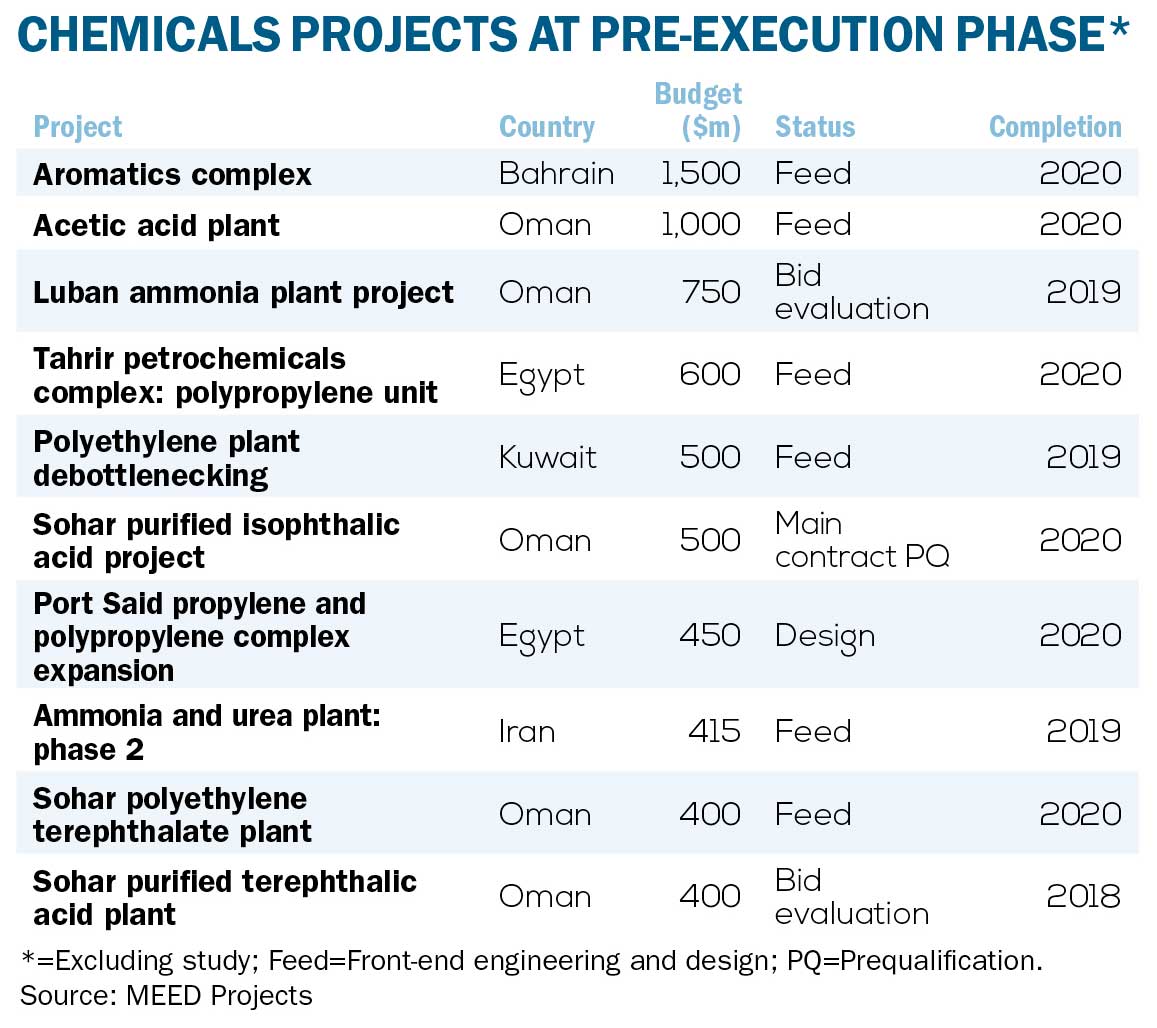

Chemicals projects at pre-execution phase

Chemicals projects at pre-execution phase

By destination, Asia accounted for 58 per cent of total GCC chemicals exports in 2015. Sales within the GCC were the second-biggest component, representing 10.9 per cent of the total, followed by Western Europe and Africa, with 9.7 per cent and 9.2 per cent respectively.

Industry leaders say GCC producers need to rethink how they can achieve the scale of some of the larger international players and maintain or even grow their market share, especially in Asia, where demand is expected to double by 2030.

Partnerships key

Sultan al-Jaber, CEO of Abu Dhabi National Oil Company (Adnoc), says partnerships with other GCC and foreign chemicals producers will be the key to survival in todays competitive market. Adnoc plans to almost triple its petrochemicals production from 4.5 million tonnes a year (t/y) to 11.4 million t/y by 2025. To achieve this, we will seamlessly integrate our petrochemicals and refining businesses, he told the GPCA forum.

[Adnoc] will seamlessly integrate [its] petrochemicals and refining businesses

Another component of Adnocs strategy is to expand feedstock used to include naphtha, which Al-Jaber hopes will change the firms cost base, drive operational efficiencies, optimise the production process and enable it to exploit the full portfolio of derivatives for naphtha to maintain strong margins. The companys new projects will focus on gasoline and aromatics production, as well as adding polyolefins capacity, which will help it increase its share in markets such as Asia.

Saudi Aramco has its own plans to almost triple chemicals production to 34 million t/y by 2030, from 12 million t/y today. Developing the petrochemicals sector is part of Saudi Arabias Vision 2030, announced earlier this year, which aims to diversify the oil export-dependent economy and create jobs for nationals.

Aramco plans to spend $334bn over 10 years across the oil and gas value chain and it has been integrating its refineries with petrochemicals infrastructure to accelerate the development of its downstream business.

GCC chemicals sales revenues

GCC chemicals sales revenues

This year, Aramco started up the Middle Easts first mixed-feed cracker. Sadara Chemical Company, the $21.3bn joint venture with the US Dow Chemical, will comprise 26 production units when completed. Of these, 14 will deliver products that have never been made in Saudi Arabia before. Aramco is also expanding its PetroRabigh complex, which it has jointly developed with Japans Sumitomo Chemical. That facility is integrated with a refinery on the Red Sea coast.

Saudi Arabia is the biggest player in terms of petrochemicals sales in the GCC, accounting for more than 63 per cent of the revenues generated by the six states. It has announced a plan to build an estimated $30bn oil-to-chemicals plant, the first of its type in the Middle East. However, the project that the kingdom hopes will strengthen its position as the top GCC producer is still some years away. The study is only expected to be finalised in the second half of 2017.

You might also like...

Hassan Allam and Siemens confirm Hafeet Rail award

24 April 2024

UAE builds its downstream and chemical sectors

24 April 2024

Acwa Power eyes selective asset sales

24 April 2024

Bahrain mall to install solar carport

24 April 2024

A MEED Subscription...

Subscribe or upgrade your current MEED.com package to support your strategic planning with the MENA region’s best source of business information. Proceed to our online shop below to find out more about the features in each package.