There are an estimated $293bn-worth of planned and unawarded projects in the oil, gas and petrochemicals sector in the Mena region, excluding Iran

With more than 40 per cent of global crude oil reserves and a fifth of its gas deposits, the Middle East and North Africa (Mena) region is one of the worlds leading hydrocarbons projects markets.

The need to meet rising local and international energy demand has driven high levels of investment in oil and gas capital projects in recent years, with more than $244bn of major contracts awarded from January 2011 to November 2016. These investment have cemented Saudi Arabias position as the most influential global oil exporter and propelled Qatar into the top spot for both liquefied natural gas (LNG) and gas-to-liquids (GTL) production.

But spending on oil and gas schemes in the region contracted abruptly in 2016 as a result of the collapse of oil prices. Brent crude fell from more than $114 a barrel in June 2014 to below $27 a barrel in January 2016. The consequent fall in oil export revenues has put significant pressure on government finances, leading to a review of spending priorities by the regions oil exporters.

Lowest spending

As of the start of December, 2016 was on course to be the lowest-spending year since 2008. About $29.7bn of engineering, procurement and construction (EPC) contracts had been signed in the first 11 months of the year, compared with $48.6bn for the full year of 2015 and $60.4bn for 2014.

As ever, the health of the projects market will remain closely tied to a handful of very large schemes proceeding on schedule as well as the outlook for oil prices, as governments weigh up whether or not to push ahead with major spending plans at a time of lower revenues.

There are currently an estimated $293bn-worth of planned and unawarded projects in the oil, gas and petrochemicals sector in the Mena region, excluding Iran. The UAE and Saudi Arabia have the largest future projects markets, with $66bn and $51bn of schemes respectively.

Saudi Arabia had the regions largest oil, gas and petrochemicals market in 2011-16, with a total of $69.37bn of deals let, accounting for more than a quarter of the regional total. The bulk of these awards, however, were in 2011 and 2012, with more than $47bn spent in these two years combined. Average spending dropped considerably in the subsequent four years.

Saudi Arabias project pipeline is buoyed by the regions two largest projects, both of which are at an early stage: Saudi Basic Industries Corporations (Sabics) oil-to-chemicals project and Saudi Aramcos integrated refinery and petrochemicals development, both at Yanbu on the Red Sea coast. These projects aside, Aramco is likely to prioritise schemes to expand its gas capacity, which includes higher gas processing capacity, the development of non-associated gas fields in the Gulf and expanding shale gas production in the north.

Kuwait returns

With capital spending on oil and gas projects of about $44.3bn, Kuwait was by far the biggest spender over the past two years after a slump in project spending at the start of the decade. That was driven by major projects such as the Clean Fuels Project, the New Refinery Project and the Lower Fars heavy oil handling facilities.

Kuwait is only number five, however, in terms of pre-execution project value. This includes the estimated $7bn Olefins 3 project and phases two and three of the Ratqa Lower Fars Heavy Oil scheme.

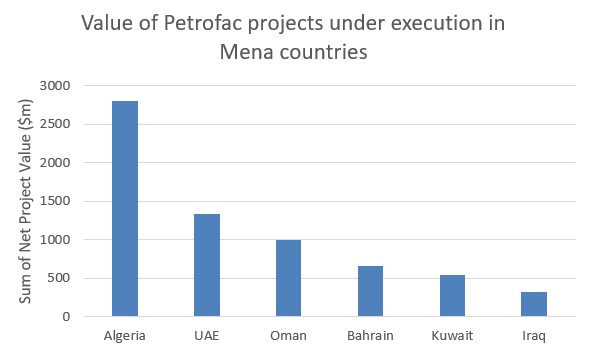

Over the period in review, the UAE was the third-most valuable market for hydrocarbons projects, spending $35.1bn. Abu Dhabi in 2013 and 2014 awarded a string of contracts in the offshore oil sector. The UAE had quiet years in 2015 and 2016 as several major schemes faced delays at the main contract bid phase, including the $3bn Bab Integrated Facilities Expansion, a new refinery in Fujairah and the Fujairah LNG import terminal. In 2016, it was not in the top five countries in the region in terms of contract awards.

The UAE is also eyeing major gas capacity expansions in the coming years, largely by developing new sour gas reservoirs. These include major projects on the Bab and Hail fields as well as the expansion of the Shah gas field.

Iraq was the second-biggest spender in 2014, with a total of $13.4bn, but contract awards declinedy in 2015 and 2016. The country has been significantly affected by the drop in oil prices and ongoing political instability, particularly in its north and west. Iraq has the third-largest project pipeline, at $47bn, but question marks hang over many of its large schemes to due budgetary constraints and security threats. Its largest schemes include the Iraq Strategic Crude Oil Export Pipeline and several greenfield refinery projects, all of which have been delayed for several years or recently announced. Upstream schemes backed by international oil companies will depend on payments from the government, which have been delayed as lower crude prices hit government spending.

Valuable sectors

In 2011-16, oil refining was the most valuable sector, with a total spend of $52.8bn, representing more than a fifth of total project awards value. The second-biggest sector was oil extraction, with $48bn, and largely driven by countries expanding crude production capacity, including the UAE, Iraq and Kuwait. Spending on petrochemicals plants dropped over the past three years, but totalled about $33.5bn.

In terms of a subsector breakdown of future projects, the largest sector is petrochemicals, with more than a quarter of total schemes planned. Many projects in this sector, however, are at an early stage and the current market environment for petrochemicals is not strong. The future of many of them also depends on the availability of feedstock, which has held back many GCC petrochemicals projects in the past. Oil refinery projects rank in second place, with the announcement of several new refinery schemes in Iraq boosting the sector. Spending is also anticipated on new refineries in Bahrain and Oman.

In terms of investments, Saudi Aramco was the biggest oil and gas project sponsor in the region in 2011-16, awarding an estimated $38.8bn of major contracts directly, with more work being handed out by its downstream joint ventures. Kuwaits upstream and downstream leaders were the second and third-largest clients in the six-year period. Kuwait National Petroleum Company (KNPC) and Kuwait Oil Company (KOC) awarded $30.9bn and $13bn of deals respectively. Abu Dhabi Marine Operating Company (Adma-Opco) remains fourth on the list due to a string of major contract awards on offshore oil field developments over 2012-14.

Mena Oil and Gas 2017 report

Mena Oil and Gas 2017 report

Gain access to MEEDs Mena Oil and Gas 2017 report by clicking here

You might also like...

Oman secures 1.5GW contract renewals

08 May 2024

Oman extends 1GW wind prequalification

08 May 2024

A MEED Subscription...

Subscribe or upgrade your current MEED.com package to support your strategic planning with the MENA region’s best source of business information. Proceed to our online shop below to find out more about the features in each package.