Industry leaders have warned that inefficient manufacturers in the region could go out of business if reforms are not implemented

The Middle East steel industry has been an important element in the economic diversification of oil-dominated economies, but the collapse of commodity prices and floods of cheap imports have left the regions sector in turmoil.

Steel industry leaders in the region have warned that inefficient producers in the GCC could go out of business as profit margins are hit by oversupply in the market.

Unreasonable export-driven policies, especially from China, have driven steel prices down to 2004 levels, said Saeed al-Romaithi, CEO of the UAEs largest steel producer, Emirates Steel.

The gap between steel production and consumption in China has widened the Chinese are not going to slow down their export drive any time soon, said Al-Romaithi, speaking at the Middle East Iron & Steel conference in Dubai in December.

China increase

Chinese steel exports to Arab countries grew by 80 per cent in 2014 and are expected to have risen by another 40 per cent in 2015, according to Al-Romaithi, who added that prices had fallen 50 per cent since 2013.

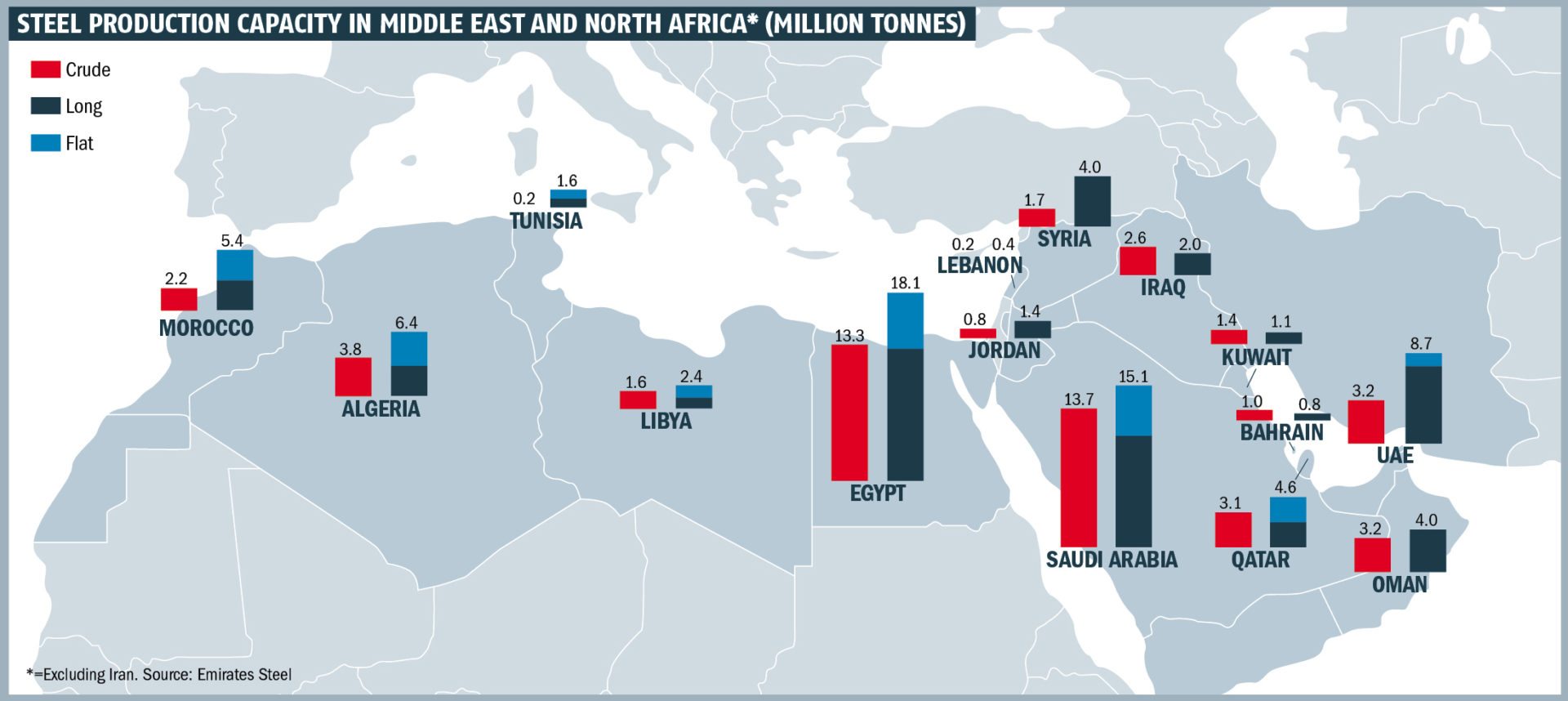

The Arab world has the capacity to produce 53 million tonnes a year (t/y) of steel and 58.7 million t/y of finished integrated products, but capacity use is languishing at under 40 per cent.

Capacity in the region grew 12 per cent over the past two years and is expected to increase another 8 per cent by 2018.

The construction sector dominates steel demand in the region, accounting for 90 per cent of consumption. In 2015, the Arab world produced 28 million tonnes of steel, but imported 27 million tonnes.

The Arab world is a significant importer despite the regions finished steelmaking capacities being able to meet regional demand.

Direct reduced iron-based (DRI-based) steel industries in the Middle East have not felt the benefit of lower energy and raw materials prices to the same extent as other regions. Energy prices have increased due to subsidy cuts, while DRI-grade pellet prices were maintained by large suppliers, despite the drop in global iron prices.

Preventive action

Al-Romaithi called for the regions steel producers to reduce their dependency on strong DRI-grade suppliers, maximise labour productivity and pursue energy-saving measures and value-added products.

At the same time, he called for governments to safeguard the sector with anti-dumping duties and import quotas, while improving certification and quality control.

If the market and policies do not change, some companies in the region face the prospect of potentially going out of business.

It is too difficult for producers something must be done. We are requesting balance, an even playing field, Al-Romaithi said.

Crude steel production in the Middle East dropped by nearly 15 per cent in November compared with the same month in 2014, according to the World Steel Association (worldsteel), which tracks output in Iran, Qatar, Saudi Arabia and the UAE.

Production for the first 11 months of 2014 fell by 1.7 per cent to 25.2 million tonnes. The total output for 2014 was 28.1 million tonnes.

Steel production in Egypt, Algeria and Morocco also dropped in the first 11 months of 2015, with Libyan output showing a recovery.

Saudi demand

Steel demand growth in Saudi Arabia is expected to slow over the next decade, in line with activity in the construction industry, according to Abdullah al-Zahrani, an analyst at Riyadh-based chemicals and metals producer Saudi Basic Industries Corporation (Sabic).

He forecast that steel demand is expected to increase by an average of 2.6 per cent a year up to 2025. This compares with average annual growth of 7.4 per cent between 2006 and 2014.

The construction sector consumes about 95 per cent of steel in Saudi Arabia. While this is expected to decrease due to demand for automotive products and steel plate, construction will continue to dominate consumption.

According to Al-Zahrani, the construction sector is expected to grow by 3.8 per cent a year between 2014 and 2025, dropping from an average of 7.2 per cent from 2005 to 2014.

Saudi Arabia was the third-largest producer of crude steel in the Middle East and North Africa in 2015, behind Iran and Egypt.

Despite slower demand growth predicted in the regions largest economy, the Middle East is forecast to be one of the worlds fastest-expanding regions for steel.

According to worldsteels short-range outlook for steel demand, Middle East consumption is expected to expand by 4.3 per cent in 2016 after respective increases of 4.5 per cent and 4 per cent in 2013 and 2014. This would make it the second fastest-growing region globally after Africa, which is forecast to expand by 6.2 per cent in 2016.

Despite robust demand growth, Middle East producers will continue to face strong competition from imports, especially as slower demand growth in China pushes additional Chinese supplies onto the global market.

You might also like...

UAE bank asset quality hinges on property market

03 April 2026

Safety and security matters

03 April 2026

Saudi forecast remains one of growth

03 April 2026

A MEED Subscription...

Subscribe or upgrade your current MEED.com package to support your strategic planning with the MENA region’s best source of business information. Proceed to our online shop below to find out more about the features in each package.

Take advantage of our introductory offers below for new subscribers and purchase your access today! If you are an existing client, please reach out to your account manager.