With the backlog mounting, the GCC projects sector is showing strong signs of recovery

It is difficult to overestimate the impact of the growth of the projects market on the six GCC economies over the past decade. Since 2003, more than $1.1 trillion of contracts have been awarded as the regions governments have transformed the skylines of their cities.

Visitors coming back to major cities such as Doha, Riyadh and Dubai after 10 years away must hardly be able to believe the scale of the transformation over such a short period of time.

Increasing awards

From just $45bn-worth of deals in 2004, the region has grown to consistently award more than $100bn-worth of contracts every year since then. Driven by increased revenues from oil sales, the six GCC states have been able to use their budget surpluses to implement their infrastructure visions. This, in turn, has created hundreds of thousands of new jobs in the construction sector and beyond.

The evolution of the GCC projects market can largely be divided into two separate phases. During the period 2005-08, the market was largely driven and dominated by investments in real estate, particularly in Dubai. However, since the late-2008 real estate crash, when prices fell by as much as 60 per cent and hundreds of schemes were cancelled, the market has seen a much larger proportion of non-civil projects that are inherently less speculative and more likely to go ahead.

Encouragingly, the fact that the projects market went up in 2009 and 2010, despite the property crash and the global recession, indicates its relative resilience to economic trends and underlines the strong impact oil prices have on project investment as a whole.

On the other hand, the past two years have seen declines in activity to the extent that, at $110bn-worth of contract awards, 2012 was the worst-performing year since 2005. The question most frequently posed by those in the projects industry is whether this decline is permanent or whether it is a short-term blip in the overall regional projects markets performance. As the global economy and regional economies recover, the indications are that the latter appears to be the case.

Indeed, 2013 has been very positive. As of November, more than $115bn-worth of deals had been awarded, with several billion more due to be awarded by the end of the year most notably deals on the UAEs federal railway phase 2 and Mafraq-Ghweifat highway, and the Doha Metros Gold Line. The market is therefore going to rebound strongly from its 2012 low. The latest MEED Insight forecast is for the year to end at about $120bn of awards, which implies growth of just under 10 per cent on the 2012 figure.

There are reasons to remain optimistic for the short and long term. There is a clear link between rising oil prices and the increase in project activity across the region. As revenues from crude sales have risen, so too has the respective governments ability to finance their schemes. Given that the majority of projects are state-funded, the oil price is crucial for the continuing health of the projects market.

Oil support

Recent global economic challenges have resulted in falls in the oil price. Nonetheless, as it hovers around the $100 a barrel mark, crude has shown a remarkable resistance to the slowdown, which bodes well. Even if the price were to fall to $80 a barrel, that would still be considerably higher than the average price six years ago, and still provide plenty of funds for the countries of the Middle East many of which have built up a large surplus in the intervening period to invest.

But oil is by no means the only driver of project activity. Demographic growth has been equally key in the development of schemes. Although projections depict slowing growth, the population of the Middle East and North Africa region is expected to more than double by 2050, to reach 600 million. Saudi Arabia and Yemen are forecast to grow around three-fold by 2050, from 30 million to 91 million, and from 25 million to 71 million, respectively. Egypt and Iran are predicted to have populations of more than 100 million in 2050.

This will result in increased demand for utilities, housing, transport facilities and social infrastructure such as schools and hospitals. Just as importantly, these types of schemes are driven by necessity rather than the speculative boom-and-bust nature of the real estate sector.

The oil price and population growth feed into economic prosperity. The economies of the region have performed remarkably well over the past decade. Qatars economy, for example, has tripled in size since 2000. Despite a short blip in 2009, most countries in the region have recovered from the global economic crisis and are recording gross domestic product growth of between 3 and 5 per cent a year on average.

As the economies grow, so too do government revenues and expenditure. State budgets have been growing each year in line with the rising price of crude. Over the coming years, as governments seek to increase spending, head off unrest and improve their infrastructure, revenues are also set to grow, much of which will be directed towards capital project programmes.

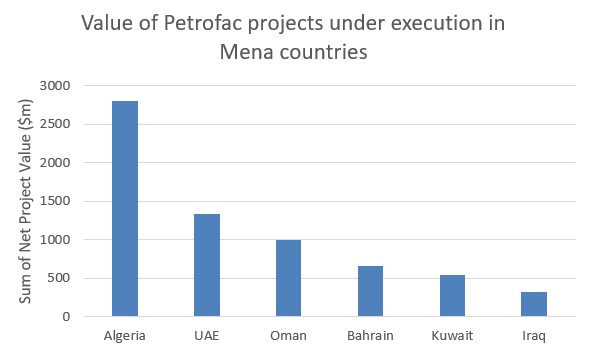

It is also important to note country-specific drivers of growth. For instance, the award of the 2022 Fifa World Cup to Qatar is a massive driver of future project activity in the state. In Iraq, the gradual return of political stability and security, along with the entry of international oil companies, are drivers that have already had a considerable impact on the local projects market.

In contrast, there are also negative political scenarios that affect the development of some projects market. Kuwait, for example, has always had great potential, but long-running squabbles between parliament and government have hindered its development.

Regional unrest

On the same theme, the impact of the Arab Uprisings on the regional projects market has yet to be fully determined. On the one hand, localised unrest and disorder has delayed project activity in the short term. On the other, the spate of revolutions has spurred governments into action, approving extra-budgetary expenditure on social infrastructure as part of an effort to head off any unrest.

Saudi Arabia, for example, has announced more than $100bn in extra funds to build low-cost housing, hospitals and education facilities as it seeks to pacify any potential discontent.

By and large, the general projects outlook for the region as a whole is broadly positive thanks to the range of drivers outlined above. The regional projects market is increasingly mature and sophisticated as it learns from its experiences. With more than $1 trillion already invested in projects over the past 10 years, there is no reason to doubt that an equal amount will not be spent over the coming decade.

Looking forwards, the total value of announced and un-awarded projects in the GCC stands at just over $1.02 trillion. This represents a substantial rise on the $788bn figure taken in mid-2012 and the $913bn in mid-2011.

Chiefly, the increase has come from an additional $150bn-worth of projects in Saudi Arabia, and $52bn-worth of new projects in the UAE. Qatar and Oman have also seen some increase in planned projects.

Over the past 12 months, some $305bn-worth of new projects have been announced in the GCC alone. New schemes include Omans national railway, part of the planned GCC railway, King Abdullah City for Atomic & Renewable Energys (KA-Cares) first two procurement rounds, and the regeneration of the Al-Ruwais district in Jeddah.

Predominant sectors

Each country continues to have a different sector focus. The UAE and Qatar, for instance, have a higher proportion of construction projects than the other GCC states, while in Saudi Arabia, which suffers from something of a power crisis, there are a greater proportion of power, and particularly renewable energy, projects. In Kuwait, a large number of future power projects predominate as the state also battles power shortages. In Oman, meanwhile, there are a larger number of water and wastewater schemes as a percentage of the total number of projects.

One of the most interesting developments over the past year has been the emergence of the power sector as the largest future sector, overtaking construction for the first time.

Almost all of this is due to the addition of KA-Cares ambitious renewable and nuclear energy programmes, which have boosted the sector by more than $200bn. It should also be noted that power sector project spending plans tend to be known years in advance, which further boosts its total compared with other sectors.

Construction is the second-largest future sector, with just over $290bn-worth of planned and un-awarded projects. This is a sizeable increase on the equivalent $217bn figure recorded last year, which highlights the ongoing recovery of the real estate market in particular.

The transport sector edges up slightly, mainly thanks to a raft of planned metro projects. It was the year of the metro in 2013, with deals awarded for schemes in Doha and Riyadh. More are to come in Abu Dhabi, Jeddah, Mecca and Kuwait.

Looking ahead to 2014, the outlook is for the projects market to build on the projected 2013 figure of $120bn-worth of contracts awarded. We anticipate that the UAE and Qatar will remain stable on 2013 figures; the former due to a revival of its real estate sector and awards for the Fujairah refinery and Abu Dhabi Metro, and the latter due to its ongoing infrastructure commitments for the World Cup.

On the other hand, we forecast the Saudi market will slip back slightly to some $54bn. The Riyadh metro awards will be taken out of the equation, while the award of other metro projects and the usual raft of power sector contracts will not be enough to offset the absence of such a large project next year.

Kuwait is set to make the biggest impression next year by virtue of $15bn-worth of awards on its Clean Fuels Project. The tenders for the three main packages on the megaproject have already been issued, with a submission date set for 24 December, ensuring they should be awarded in 2014. The addition of this one project alone could be the principal difference between the 2014 and 2013 figures.

Projects market

The region has consistently awarded more than $100bn-worth of contracts every year since 2004

Source: MEED

Ed James is the head of MEED Insight. For more information and data on the GCC and Mena projects market, please see the Mena Projects Forecast and Review 2013 report by MEED Insight (www.meed.com/research).

You might also like...

Oman secures 1.5GW contract renewals

08 May 2024

Oman extends 1GW wind prequalification

08 May 2024

A MEED Subscription...

Subscribe or upgrade your current MEED.com package to support your strategic planning with the MENA region’s best source of business information. Proceed to our online shop below to find out more about the features in each package.