With a solid track record in gold mining, the Saudi company is developing its bauxite and phosphate reserves as it seeks to become a global supplier of aluminium and fertilisers.

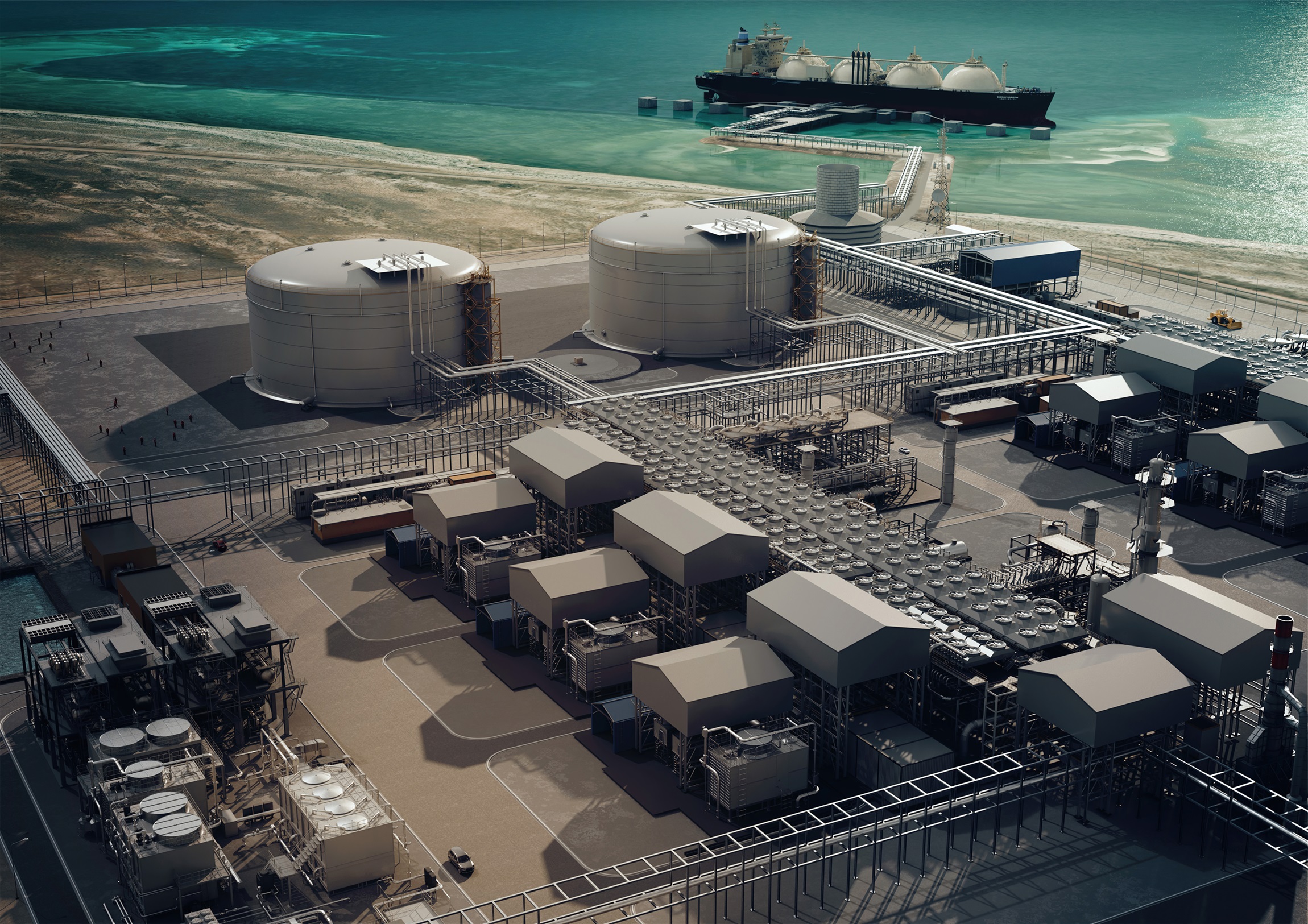

The long-term commercial prospects for Saudi Arabia’s $10bn Ras al-Zour aluminium project remain strong, despite the loss of a direct equity participation from UK/Canadian aluminium producer Rio Tinto Alcan in December 2008.

Rio Tinto has opted to offer technical support to the scheme by providing the equipment for the integrated aluminium complex rather than through an original plan of investment that would have given it a 49 per cent share in the development.

As a result of Rio Tinto’s decision, client and partner Saudi Arabian Mining Company (Maaden) is splitting the smelter’s development into two phases and taking sole responsibility for securing the project finance.

However, there is no challenge to the underlying economic rationale for developing the Ras al-Zour smelter. To be built on the Gulf coast north of Jubail, it will be supplied with alumina refined at Maaden’s bauxite mine in the northern Qassim province.

Competitive edge

By combining the cost benefits of producing its own alumina while using cheap local energy, Maaden should attain a distinct competitive advantage at Ras al-Zour, even in today’s increasingly competitive Gulf smelting sector, into which the UAE, Qatar and Oman are also expanding through smelter projects (see feature, page 38).

“When you plan a new smelter, you cannot take a short-term view,” says Massimo Rossi, senior aluminium analyst at UK consultant CRU Group. “Looking beyond the current economic slowdown, big emerging economies such as China and India will need aluminium. Saudi Arabia is well located to supply both these markets and Europe.”

Aluminium demand in the Gulf will begin to grow again once construction activity in the region starts to rebound from the current slump. Middle East producers are well placed because they have sustained access to cheap energy.

Of course, this is a bonus enjoyed by all Saudi Arabia’s neighbours. “Maaden will be entering a crowded Gulf sector,” says Rossi. “Dubal [Dubai Aluminium] and Alba [Aluminium Bahrain] are well established. Oman’s smelter began operations last year and Qatalum [Qatar Aluminium] is due to open in a few months’ time. The Emal [Emirates Aluminium] plant is planned for Abu Dhabi and some of the smelters are also planning second phases that would increase production even further.

“But the Ras al-Zour plant will benefit from one distinct advantage over these local rivals: it will have access to its own supplies of refined alumina. Control of the alumina and bauxite resources is important. This point is also reinforced by a proposed deal between Dubal and Brazil’s Vale Mining Company, on the basis of which the Middle East aluminium producer would acquire a 19 per cent stake in Brazil’s Companhia Alumina do Para.”

The withdrawal of Rio Tinto Alcan as a potential shareholder has forced Maaden to spread costs by relying on imported alumina for phase one of the project until it can secure the remaining financing to complete its own bauxite mine and alumina refinery at Zubairah, in Qassim. But this transitional period should be relatively short, the exact period depending on the banking market’s readiness to finance the second phase.

One further complication is that the quality of the bauxite produced in Qassim will have a significant impact on the economics of the Ras al-Zour smelter. If the bauxite proves to be low-grade, it will push up the cost of production.

Maaden’s decision to split the development into two phases is based on the company’s wider development strategy. Not only is the group seeking to expand its existing gold mining and exploration activities, but it is also engaged in the development of a $5.5bn scheme to develop phosphate reserves at Al-Jalamid, near Turayf in the far north of the kingdom, as the source of raw material for a huge new fertiliser plant.

Maaden’s gold strategy is focused on three main themes: extracting the maximum return from existing mines at Al-Amar, Bulghah and Sukhaybarat; pushing forward the central Arabian gold project, which covers a collection of potential mines; and sustaining exploration programmes, particularly in the centre and north of the kingdom.

Like the aluminium smelter, a fertiliser plant will be located at Ras al-Zour, and will be serviced by a new rail spur from the mining operations in the Arabian interior, financed by the government’s Public Investment Fund, which was set up in 1971 to facilitate the development of the Saudi economy.

Saudi Basic Industries Corporation (Sabic) is a 30 per cent minority partner in the Al-Jalamid project, making Maaden legally responsible for the $3.8bn project financing put in place to support the development in July 2008.

The consortium’s initial success in raising such a large sum -almost half of it sharia-compliant -as the credit crunch began to bite was an encouraging signal of market confidence in the prospects for Saudi Arabia’s fledgling minerals industry. But of course, in assuming such a high level of debt, Maaden has placed itself under pressure to deliver strongly in commercial investment terms.

The fertiliser venture is targeting the world market, with capacity to cater for up to 20-25 per cent of forecast global demand for phosphate fertiliser, Sabic has claimed. The plant will be able to produce 3 million tonnes a year (t/y) of diammonium phosphate fertiliser, together with 4.5 million t/y of sulphuric acid, 1.1 million t/y of ammonia and 1.5 million t/y of phosphoric acid.

The domestic Saudi agriculture sector will provide some demand, although this may be hard to forecast following Riyadh’s decision in the summer of 2008 to gradually phase out water subsidies for the kingdom’s wheat farming industry, and some of the phosphoric acid will be sent to the Sabic-owned Ibn Albaytar fertiliser plant in nearby Jubail.

However, international markets will be a prime sales target for the operation. The global downturn threatens levels of demand for Maaden’s planned output of phosphates and aluminium, as with almost any major commodity production project at the current time.

But the company may be fortunate in the timing of these projects. Development work is still at a relatively early stage. By the time the facilities come into full production, global economic activity may have begun to recover, reviving demand and prices for major industrial commodities.

Indeed, the global economic downturn has provided one benefit: the fall in international engineering and construction prices as contractors find themselves with spare capacity. This has opened up the prospect of major savings for the aluminium scheme.

Two years ago, with the world project market booming, the cost of the Ras al-Zour aluminium project was forecast at more than $10bn. Now the forecast cost has fallen to about $8bn. The US’ Bechtel Corporation, which won the contract for engineering, procurement and construction (EPC) and management (EPCM) on the aluminium smelter in October 2008, is currently working on a new assessment of the cost of developing the first phase of the project, following a fall in EPC prices over the past six months.

Unfortunately, Maaden is unlikely to reap similar benefits on its fertiliser scheme. The company confirmed in the summer of 2008 that capital development for the venture had been contracted at a fixed rate under lump sum turn-key contracts for the EPC of both the beneficiation and processing plants, and the supporting infrastructure.

Maaden and Sabic are contributing 30 per cent of the budget in the form of their equity stakes in the joint venture company created for the project, Maaden Phosphate Company. The balance is coming from the syndicated financing signed in June 2008 with a consortium of local and international institutions, with the UK’s Standard Chartered Bank and Saudi Arabia’s Riyad Bank acting as lead advisers.

Growing business

The scale of Maaden’s plans -the phosphate venture will be one of the world’s largest -contrasts sharply with the relatively small dimension of its existing mine operations, for which last year’s capital expenditure was projected at just $10.6m. The group is an established, but small, producer of gold and other by-product metals, including silver, copper and zinc.

But while this arm of the business -concentrated in the west and centre of the kingdom -may not compare with the ambition of the big northern projects, it has played a pivotal role for Maaden. In developing and operating a series of small gold mines, the company has been able to establish a track record of performance. That was clearly helpful when it set out to convince potential financing banks of its capacity to effectively manage the phosphates project.

In contrast to oil, petrochemicals, steel or banking, mining is not a sector where Saudi Arabia has a strong position. But thanks to its gold business, Maaden cannot be labelled a novice. Indeed, the group has signalled its awareness of this by releasing into the public domain a detailed independent expert’s report on Maaden’s goldmining and exploration assets.

The authors, UK-based SRK Consulting, point out that Maaden started out by commissioning a zinc plant in 1997, at Mahd Ad Dahab, before moving on to open gold mines at Al-Hajar, Bulghah and Al-Amar. Another mine, at Ad Duwayhi, is under development, while further prospects at Mansourah, Ar Rjum, Masarrah, As Suk and Zalim have been under consideration.

The schemes constitute the central Arabian gold project, through which Maaden hopes to push gold equivalent output up to 250,000 ounces by 2011 and 500,000 ounces by 2013. Altogether, the group has 17 prospects, particularly in the north, in its exploration portfolio.

Recent high gold prices -provoked partly by investors seeking safe havens of value at a time of global economic turmoil -have created a favourable environment for the development of new prospects. However, the SRK study, completed in late 2007, identifies several shortcomings in Maaden’s gold portfolio. It notes that no environmental impact assessments have been carried out for Sukhaybarat and Mahd Ad Dahab, and points to a failure to prepare mine designs and production schedules more than one year in advance.

SRK’s comments suggest that Maaden could learn some useful lessons from mining companies elsewhere about how to make the most of its gold resources. But by submitting itself to such external analysis, and releasing the results into the public domain, the Saudi group has demonstrated a willingness to learn from the experience of others as it prepares to embark on the phosphate and aluminium operations that could transform the scale and nature of Saudi Arabia’s mining industry.

You might also like...

QatarEnergy awards $121m refinery turnaround contracts

24 March 2026

Morocco port operator approves $2bn investment programme

24 March 2026

A MEED Subscription...

Subscribe or upgrade your current MEED.com package to support your strategic planning with the MENA region’s best source of business information. Proceed to our online shop below to find out more about the features in each package.

Take advantage of our introductory offers below for new subscribers and purchase your access today! If you are an existing client, please reach out to your account manager.