Despite being hit by tighter liquidity and falling government deposits, GCC banks are still generating respectable returns

Banks in the GCC are expecting weaker economic conditions to continue in 2017, but they should remain profitable. While they are being more cautious on lending as a response to deteriorating asset quality and lower liquidity, they have managed to reprice their loan books to support interest margins.

Profit growth may have slowed as a consequence of lower oil prices, but lenders are still strong and well-capitalised. In the longer term, banks need to adapt to changes in the financial world, as new regulations and technological developments put increasing pressure on business models.

Staying relevant

There will be many levers to manage in 2017, says Emilio Pera, partner and head of financial services for the lower Gulf at Netherlands-based KPMG. The biggest challenge is how to remain relevant to customers while complying with regulatory demands and investor pressure.

Banks are being forced to increase spending on financial technology, or fintech, to keep up. Competition is growing, both with other lenders and the non-bank financial services sector. Customers are demanding a more streamlined service, says Pera. Global players are offering more and more digital solutions, and there are also non-bank competitors such as crowdfunding and peer-to-peer lending to contend with.

For example, in November alone, Dubais Emirates NBD launched a beta version of a chatbot promoted as a virtual assistant, a fitness account linked to customers mobiles and wearable fitness apps, and contactless loyalty cards. The bank is investing $136m in digital innovation over the course of three years.

While these examples are customer-facing and promotional, fintech will have a deeper impact on how banks operate in asset management, back office systems and payments. Introducing new technology can also bring down staffing costs, a key concern in the weaker operating environment.

Cyber attacks

Most importantly, banks need to stay up-to-date on cybersecurity. An alleged hack in April on Qatar National Bank (QNB), the largest bank in the GCC, was widely reported. Some 1.4GB of customer data was leaked, causing significant damage to QNBs reputation. The UAEs RAKBank and Investbank are also reported to have been targeted, showing how vulnerable GCC institutions are to cyber attacks.

Banks are also under pressure from tighter liquidity in the GCC, especially in Saudi Arabia, Qatar and Oman. Interbank lending rates peaked in the second half of 2016, at 2.3 per cent for the Saudi three-month rate and 0.4 per cent for the Omani overnight rate in September.

Liquidity is clearly tighter throughout the GCC, mainly reflecting higher funding costs and slower deposit growth, says Redmond Ramsdale, head of GCC banks at US/UK-based Fitch Ratings. Funding is predominantly from customer and interbank deposits, however, as deposits are not growing as fast as in the past and are now not keeping up with loan growth. Liquidity is getting tighter.

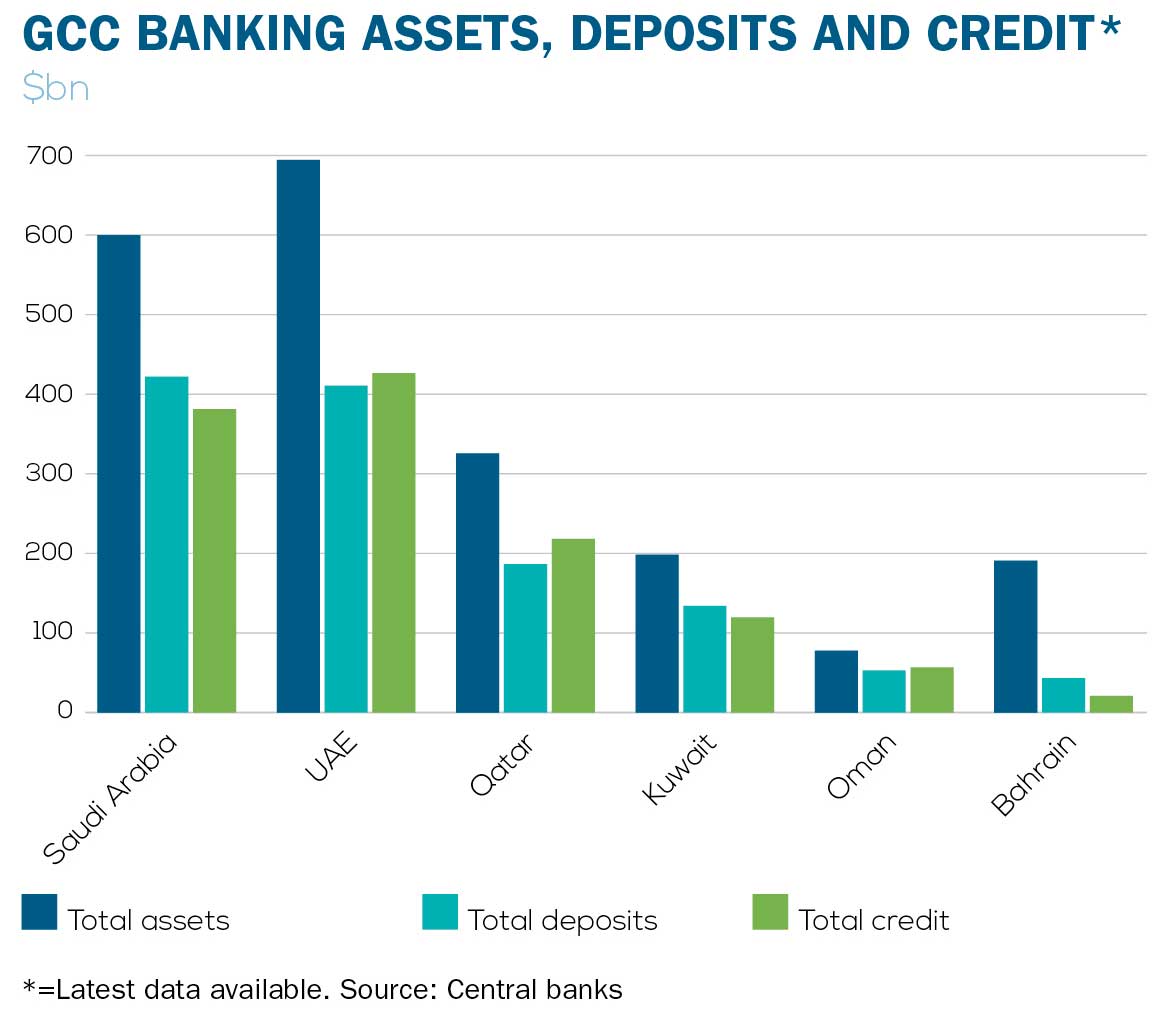

GCC banking assets, deposits and credit

GCC banking assets, deposits and credit*

Government deposits in the banking sector have slowed or fallen in 2016. The UAE had seen just 2 per cent year-on-year growth by October, while state deposits were down 12.5 per cent year-on-year in Saudi Arabia by September.

Sovereign and bank international bond issuances are bringing new liquidity into the system, but conditions will remain tight in 2017. Bank issuances in 2016 included a $500m sukuk (Islamic bond) by both Dubais Noor Bank and Dubai Islamic Bank. Kuwaits Burgan Bank raised $500m in conventional bonds, while National Bank of Abu Dhabi (Nbad) issued a $621m Formosa bond in Taiwan and QNB issued $1bn under its euro medium-term notes programme.

In terms of issuance, the likes of Emirates NBD and Nbad are well positioned, due to their strong track record of issuance, and large and diverse investor base, says Ramsdale. They can raise funding quickly, but for smaller banks it is a slower process, with many of them currently updating euro medium-term note programmes so they are ready if liquidity tightens more.

Cost of borrowing

Banks recourse to market funding is in turn pushing up the cost of borrowing for consumers, as lenders reprice to maintain interest margins, all the more important since the US Federal Reserve hiked interest rates. However, with large cost-free deposit bases, many GCC banks can only benefit from rising interest rates.

The weaker economic environment is compounding the liquidity issue, slowing demand for lending from the double-digit growth seen in 2014, except in Qatar. Loan growth continues to outpace deposit growth in the GCC, and loan-to-deposit ratios (LDRs) have been stretched to reach 116.9 per cent in Qatar and 106.9 per cent in Oman in September.

Lenders are also tightening their underwriting policies. Banks are carefully considering how to deploy their funds, says Pera. They are looking at exposure and concentration risk in their portfolios.

While the pace of government spending cuts is expected to moderate in 2017, banks will see a weaker operating environment, which will weigh on asset quality. Although non-performing loan (NPL) ratios are as low as 1.2 per cent in Saudi Arabia, sector concentration is increasingly a concern.

Asset quality has been stable to date, as impaired loans have been benefiting from strong loan growth, says Ramsdale. We expect a fall-off in loan growth, portfolios will season quicker and there could be an uptick in impaired loan ratios. We believe it will be minor, but in Saudi Arabia the deterioration could be faster, as lending growth has fallen more quickly and we have seen stress in the contracting space. That is a concern, and with the high concentration it may filter into asset quality overall.

GCC banks are heavily exposed to single borrowers and the construction and real estate sectors. These are struggling amid falling capital spending, delayed payments by governments and weak real estate markets, which also affect the value of banks collateral. All these factors mean profits are under pressure. Nonetheless, GCC banks are still generating respectable returns despite the slowdown, and can cover loan impairments.

Diverging markets

? The UAE is the largest banking market, but banks suffer from stiff competition, compressing profit margins. There are also high levels of legacy NPLs from the 2008 real estate crisis. The NPL ratio fell to 6.2 per cent by the end of 2015, but is expected to creep up as weaker growth hits smaller enterprises.

? Saudi Arabia has seen a sharper growth slowdown than other GCC countries and liquidity has tightened. The kingdoms banks are still the most profitable in the region, however, with a 2.1 per cent return-on-assets (ROA). The Saudi Arabian Monetary Agency has taken several measures including liquidity injections and increasing the LDR ratio cap to 90 per cent. Severe delays in government payments have put pressure on contractors, forcing loan restructuring.

? The Kuwaiti government spent more in 2014 and 2015, stimulating economic growth. This gave banks new opportunities to lend, and credit was up 7.5 per cent year-on-year by September 2016, while liquidity remains good.

? Economic growth has slowed less in Qatar than in other GCC states, and credit growth has remained high, reaching 12 per cent year-on-year by September. ROA is still high at 2 per cent. However, with the slowdown in deposits, the LDR shot up to 116.9 per cent, despite incoming regulations that limit it to 100 per cent.

? Bahrain banks have suffered from low profitability, with the ROA ranging from 0.5 per cent for wholesale Islamic banks and 0.1 per cent for retail Islamic banks. This overbanked market would benefit from mergers of smaller banks. The LDR is just 48.6 per cent, while system assets fell 0.8 per cent year-on-year by April.

? Oman is experiencing tight liquidity, with credit growing at 11 per cent and deposits at just 4.9 per cent a situation that is likely to persist.

You might also like...

Diriyah’s continued era of culture and commerce

22 May 2026

Hoping for a long, cool summer

22 May 2026

A MEED Subscription...

Subscribe or upgrade your current MEED.com package to support your strategic planning with the MENA region’s best source of business information. Proceed to our online shop below to find out more about the features in each package.

Take advantage of our introductory offers below for new subscribers and purchase your access today! If you are an existing client, please reach out to your account manager.